Hello

I am trying to backest binary strangle on news, with some parameters

data used :

backtest engine :

excel vba

tested on 2h contracts or 3pm daily contract

from 2010 to our may 2017, by 2 years sections

parameters

price to buy or sell

time to get in (beetween opening contract time and news time)

TP to get out (or expiration)

parameters for Black Sholes formula

This is done and have some results, like what news are mostly profitable

But the problem is I don’t master the volatility parameter in the BS formula

I am forced to use a fixed volatility, and it is not realistic at all

Is there a way to know what volatility is used at nadex, at a particular time and day ?

I asked them twice but no answers.

Do they calculate volatility from known indicator (like VIX) that I could download and use? And with what formula ?

Also, is there other people in the forum that has tried to backtest binaries strategies ?

Regards

eric

1 Like

Unfortunatley there is not data that far back that would show the pricing of binaries at those exact times to get exact numbers, nor is there a known set indicator that the market makers use to determing the Iv and pricing etc. The best thing you can do with that type fo backtesting is to look at the amount of the typical moves on certain news events, then use those expected average moves when choosing the binary strikes and using the strike ladder to see what dollar amounts that type of move will create etc. But great job on really digging in and tracking these stats and attempting to get hard data on these strategies! That is awesome

Thanks skeltonmark for your answer

For the entry (strangle strategy before a consequent news)

If I understand, I could get the average move of a currency on a specific news, and it will help me to choose which strikes I buy and sell. But I don’t see how can I obtain the price of those bought and sold positions.

Of course I can use the BS formula, but again I need a volatility to make is works.

Is the volatility in the option prices rising long time before the news (1 hour ? just 15mn ?)

For the exit, it is a little less tricky

- I could skip the formula (and the volatility problem) if I exit at expiration (don’t like that too much),

- If could exit at 50 : if I understand, ATM option are priced around 50 regardless volatility and time (before expiration), right ?

- if I want an OTM/ITM limit exit (say 20 for the sell / 80 for the buy), I have to use the BS formula and the volatility. But I have the feeling that the pricing is less sensitive to volatility as expiration approaches (can you confirm that , or is it just the opposite !).

- also, I can force an exit to be enough far from the news, in that case the volatility will have dropped (right ? , is that dropping 15mn after, 1 hour ?)

So it is more the entry that annoys me

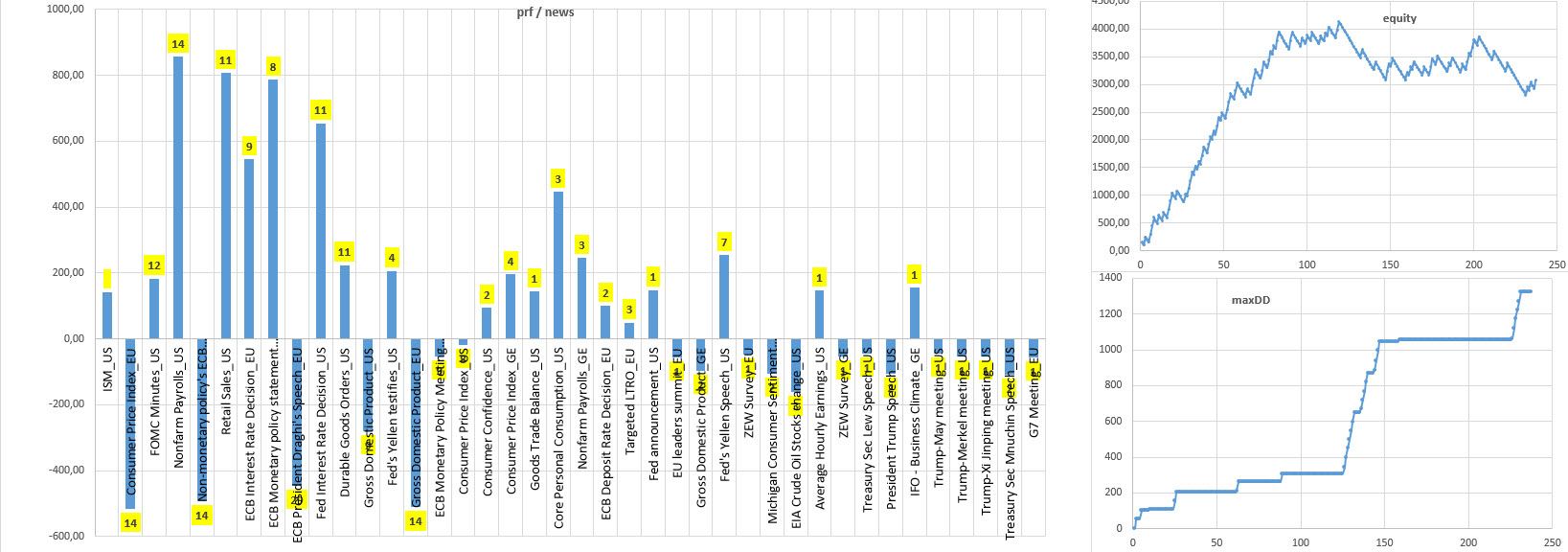

Here is are some examples of backtest

(to be taken with caution : may have some bugs, and option price aren’t priced as in realtime)

BT 1

EURUSD, jan2016-may2017, 1’ forex data, all red (US and EU) news (www.fxstreet.com/economic-calendar)

two “2_hours_contracts” (divide by 2 for one contract)

entry : one minute before the news with OTM options (less that 15usd and more than 85 usd)

exit : at expiration

about the tricky parameter : volatility (for black $ sholes formula) , a simple model :

- 12% before time_of_news + 2 minutes

- 9% beetween 2 mn and 10 mn after news

- 7.5% beetween after 10 minutes after the news

(increasing V decreases the results as OTM options are farther away ; 12% is not realistic for strong news)

yellow numbers = number of trades for a specific news during the period

BT 2

like BT1 but filtered with the most important news

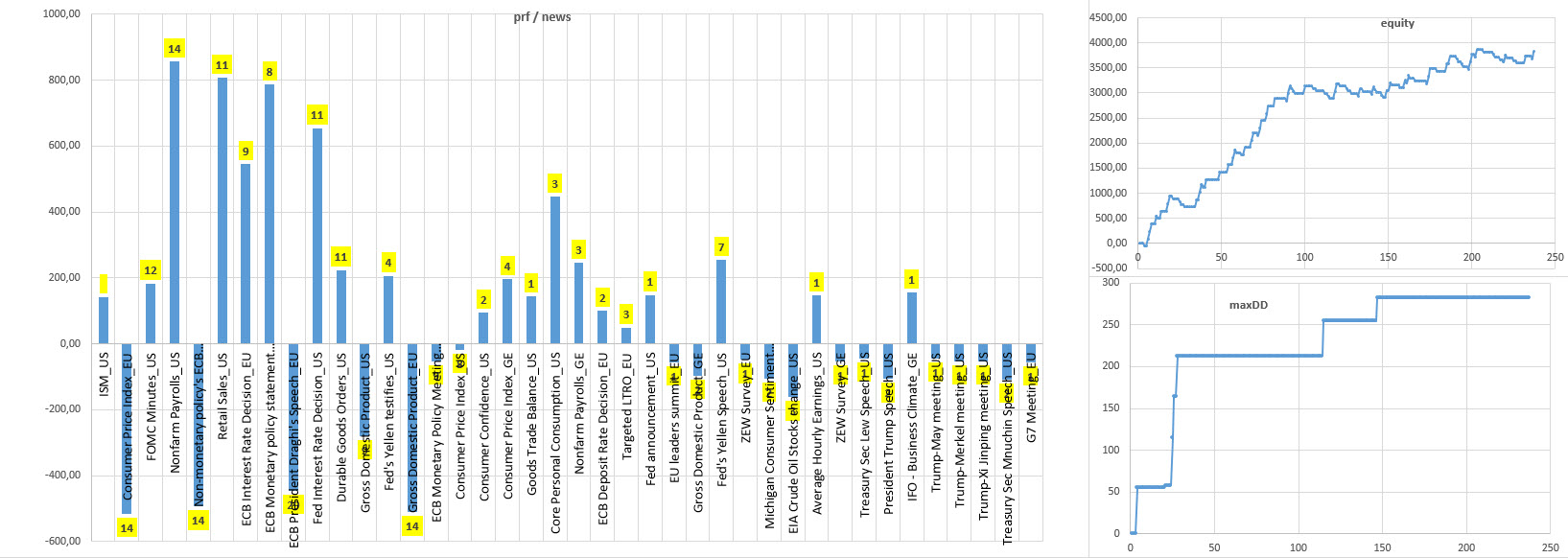

BT 3

everything like BT1 but exit

exit : one leg if option price is more than 90 for a buy, less than 10 for a sell (or at expiration)

non filtered

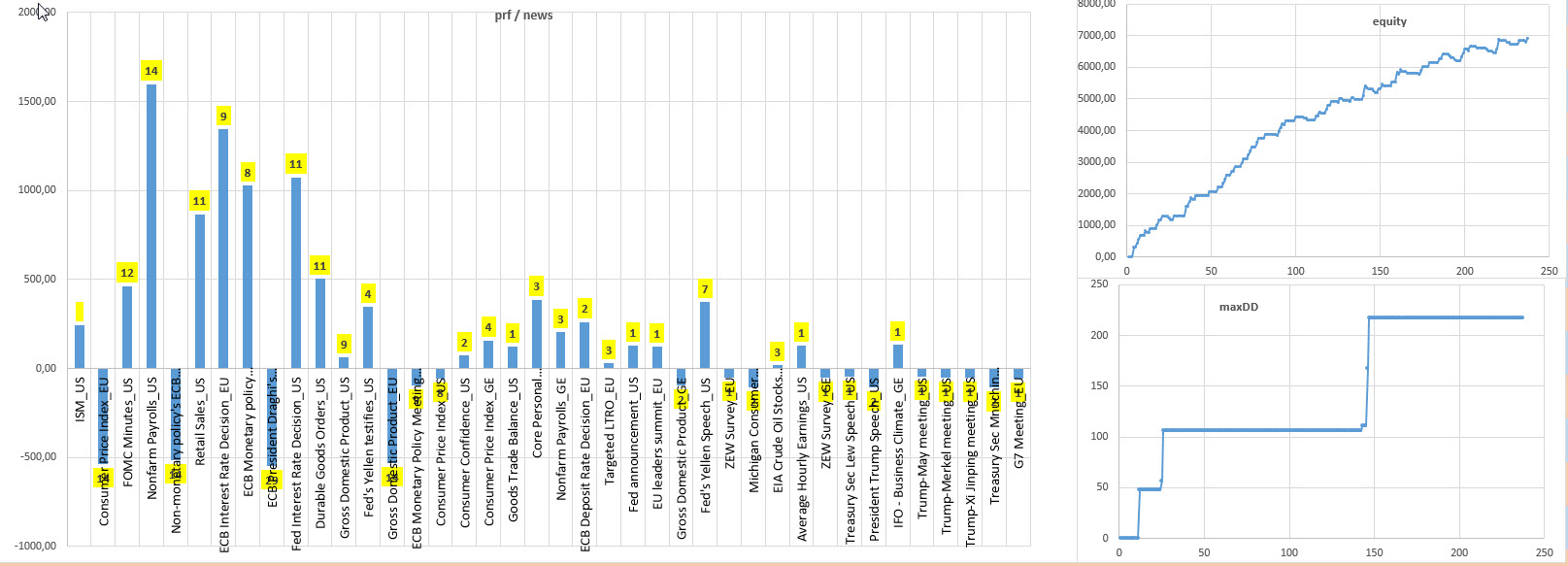

BT 4

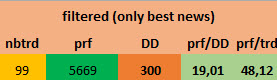

like BT3 but filtered with the most important news

The stats of B1 B2 B3 B4

It seems that exiting on TP increases the perf and decreases the drawdown (either on filtered BT or not)

Does it make sense ?

(should be tested in demo)

note :

exits_TP = number of trades that touched TP

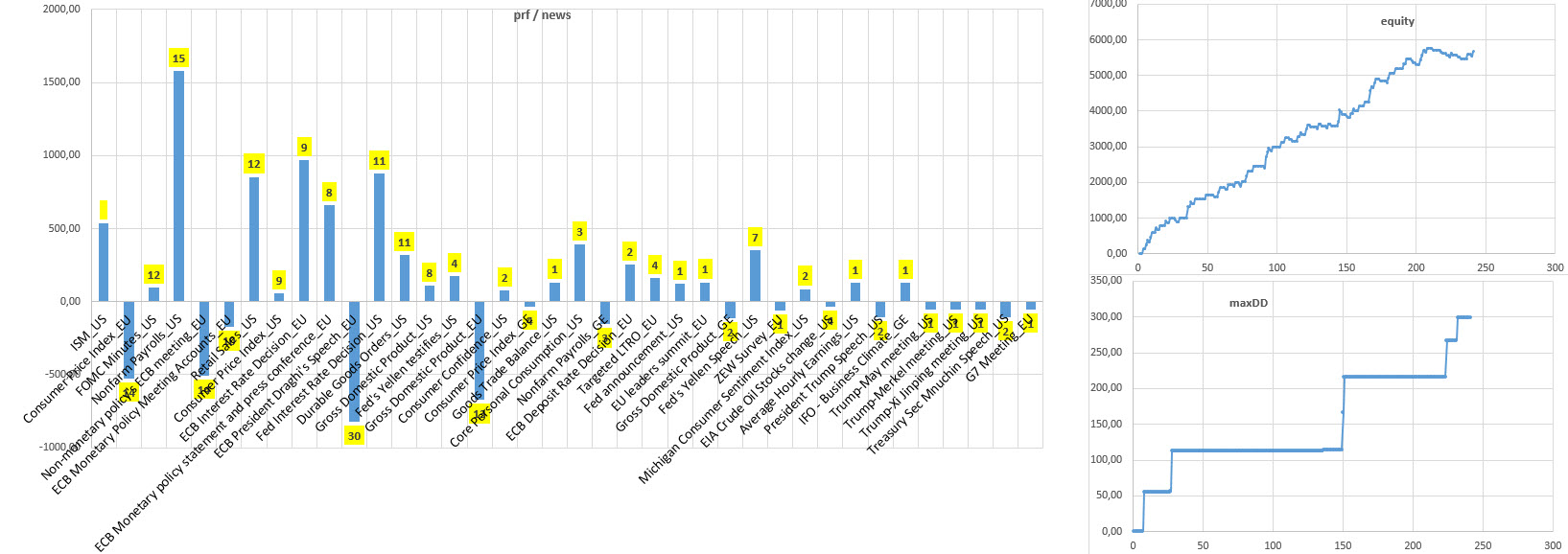

To see how the backtest depends on volatility, here is a more realistic choice of volatility model

- 20% beetween time_of_news - 2 minutes and time_of_news + 2 minutes

- 15% from 2 to 10 minutes around news

- 12.5% before time_of_news - 10 minutes and after time_of_news + 10 minutes

That is for emulating a spike of volatility (of course it would be better to have the real one)

Here is BT5, the BT4 (filtered, and TP=90/10), with that volatiliy model, and an entry 10mn before the news (before the spike)

The stats, to be compared with BT4

1 Like